What if inflation does not drop to 2%?

What if inflation does not drop to 2%?

Monetary trends drive private credit. A steeper curve will bring back the money momentum in the US, while we see diverging trends in Europe and the US.

Being away from the desk for a few days allows me to take a step back and ponder about some of the biggies in global macro. I have spent the first few evenings in Spain investigating the intriguing differences between Europe and the US in monetary terms.

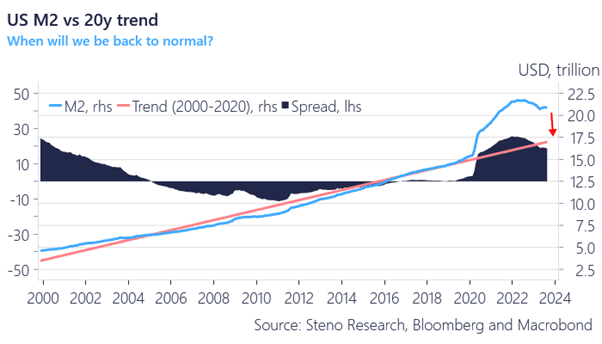

As most of you know by now, I love a bit of base layer monetary analysis. The USD M2 trend remains firmly above the trend and we even see signs of an aggregate rebound in the broad USD supply.

The supply of USDs remains 16% above trend, and with recent signs of a rebound, it seems unwise to bet against the trend from here. Private credit markets remain reasonably solid despite “tight” USD rates.

If you believe that money drives prices (we to a large extent do), then this is a (really) bad sign for intentions of bringing inflation to 2%. What if inflation will never get back to target during this cycle?

For the FULL article with conclusions for investment portfolios, follow us to https://stenoresearch.com/watch-series/money-watch-monetary-trends-scream-2-inflation-still-in-the-us/

Use “Macro30” to get 30% off your first subscription at Steno Research.

Chart 1: USD supply versus a 20-year trend