Stenos Signals #8: Outright deflation risks in 2023 are increasing

The current supply squeeze is one of the worst seen ever. The disconnect between demand fundamentals and food- and energy prices is simply eye-catching. Watch the downside, but not yet.

Happy Easter everyone!

It has been a little while since I updated you, but it seems as if politically driven supply side constraints continue to haunt across the board. Lockdowns in Asia and supply-side restrictions on energy paired with a continued stimulative fiscal- and monetary environment is just a cocktail for inflation – end of discussion.

We though need to talk about the demand side soon, because the cracks are appearing right about everywhere, which is why I stick to my view that 2023 risks being outright deflationary, but bear in mind that it is probably too early to trade that story yet.

Energy prices remain an obstacle to growth this year and political decisions still move towards constraining supply due to geopolitical reasons that I am fully aligned with. The consequence are obvious and many: The Redhen facility in Germany, which is the biggest in Northern Europe, is now 100% empty. There is simply no natural gas in the Gazprom storage facility. This is Putin’s price hike as Joe Biden has labelled it, but Putin is obviously far from being responsible for all of the inflation that we are currently faced with.

Chart 1. The Natural Gas Storage Site in Redhen is EMPTY

Food prices also surged in the most violent way that we have seen in modern history on the back of the Russian invasion of Ukraine and we know from anecdotal evidence that for example German retailers have raised prices on a pamphlet of food-related products through April as well.

This is going to get ugly for Euro zone inflation numbers this quarter, but it also comes with a clear cost on the demand side. The latter is what most analysts currently tend to forget in my humble opinion.

Chart 2. Food prices showed the most violent monthly move in modern history in March

The demand side ought to cool down materially just a consequence of the inflation seen in energy- and food prices, which are by the way two price categories that monetary policy cannot influence to any material extent.

The weekly earnings in the US are now running BELOW trend, when you adjust for the most recent price trends, which is a massive change of scenery compared to 2020 and 2021. When necessities turn more costly, it simply means that people will stop buying discretionary stuff soon. This ought to provide substantial disinflationary winds through H2-2022 and in to 2023 (Yes, I stick to that story).

This also means that the price on everything you need will remain high, but the price on everything you don’t need will start dropping soon.

Chart 3. Weekly inflation adjusted earnings are falling off a cliff

This brings me to the most important chart in global macro right now. The Chinese domestic demand is falling off a cliff due to the super lockdowns in Shanghai and other regions. The risk is sadly still tilted towards even more draconian lockdowns in other Chinese regions and commodity prices (especially those linked to industrials) rarely remain this high, when the Chinese economy is not performing.

This is the biggest disconnect between the supply and the demand side that I have seen in recent decades, and it will hence take even bigger supply constraints on commodities to prolong the current price rally. The demand side is simply not pushing the needle anymore.

Chart 4. The biggest decoupling between China and commodity prices in decades

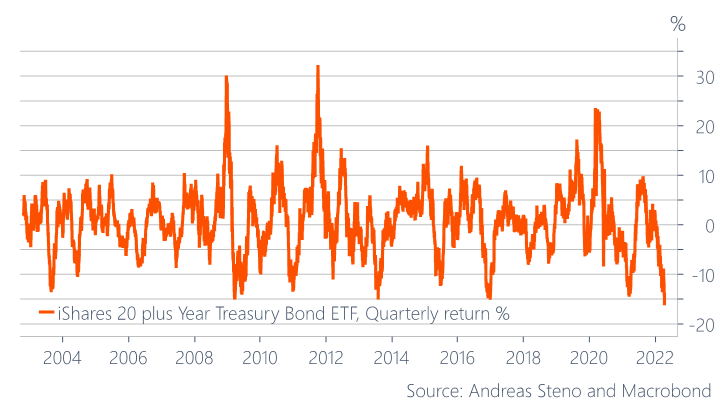

The consequence of the worst month in decades price-wise is crystal clear in bond space. This is now officially the worst running quarterly return ever in the time-series history of the 20+yr USD Bond ETF. Being a contrarian by nature this tempts me into trying to go long, but I would probably prefer to keep my powder dry on that trade until we have a clearer signal that inflation has peaked (should arrive in Q3 at the latest).

Chart 5. The WORST running quarterly return for 20+yr bonds in many decades

Instead, my preferred trade is currently to be long Consumer Staples (Wallmart, Proctor & Gamble and so on) versus Consumer Discretionary (Amazon, Tesla and so on).

Be long stuff that people need and short stuff that people don’t need for now. It is as simple as that.

Chart 6. Buy Staples vs. Discretionary

Finally, I want to remind you of the BIG launch of “The Macro Trading Floor” podcast that I am co-hosting with one of my best buddies Alfonso Peccatiello. Every week Alf and I will be joined by a guest who will present us with an actionable macro trade idea.

We will decompose the trading idea for the audience and discuss its pros and cons before deciding to go long or short in the “The Macro Trading Floor” portfolio. This is daunting stuff, folks!

Furthermore, we will have the usual banter. You might hear Alfonso fuming over somebody having ordered cappuccino after 10 am, while we will also have a segment on the ‘’worst chart of the week”.

Please help us spread the news by rating and/or sharing the show. Links to Spotify and Apple can be found below.

The premiere will air this Sunday April 17. Stay tuned!

Spotify:

Apple:

I agree that there are severe deflation forces present, especially demographic. However what you and all other deflationists always forget (and I am of the same opinion for many many years, not just in the recent year or so when inflation has became main narrative) that all deflation forces are trumped by fact that the main currencies countries can print even more money (and/or make larger deficits) than the amount of money/credit/value destroyed by deflation forces/lower speed of money circling around. I also agree there will be some tigthening of monetary conditions, as inflation expectation got too much ahead and became too noticable from public/political/investors's point of you, which will cause a temporary reccession(s) and/or stagflation down the road. But make no mistake, the main tool or maybe better say main goal of monetary policy

almost anytime anywhere in (modern) financial era has been inflating away value of debts and other liabilities. But it must not become too obvious, therefore there will be some tigthtening. And that is also the reason why true inflation data is almosts all the time everywhere underappreciated which is one of ways which enables inflating away debts. But the main reason for tightening financial conditions is the wish to cause recession in order to lower employment numbers, as power of labour became too strong in relation to capital; also had happened many times in the past, but of course noone can't admit it to wider public. I am of such opinion for many many years, but it recently former Reserve baank of Ney York Governor&Vice President of The FED Bill Dudley explained and confirmed that very clearly (but who of the labour class reads his columns in Bloomberg :-D ) and I think that even the FED president himself said clearly that labour market is too tight and therefore financial conditions have to be tightened in order to bring level of employment down.

Yes agree consumers are/will reduce discretionary spending. This is really a deleveraging of the global debt markets especially Governments using inflation. If commod and energy stays high combined with limited supply then it will take longer to see deflation - might be 2024+. I have subscribed to the podcast - cant wait to hear - many thanks