Stenos Signals #2 – Why the Pandemic is about to get disinflationary

The current inflation is mainly a result of lagged consequences of the pandemic trends, but as these trends are about to reverse, we may experience the disinflationary part of the pandemic soon.

I am one week into my career as “substacker” and I already have to admit that I have been wrong in my market narrative so far. It is hopefully better to fail early than late, why I will continue writing despite my early blunders. Last week, I told you not to bet against gravity as I found that inflation and growth would be pulled down sharply by base effects (and other things) during 2022. My view remains the same, but what I probably should have added was something about the tradeable timing of that view.

Luckily the last week has delivered some interesting news that I can use to elaborate on that exact timing. I was actually planning on writing about why the ECB will face an immense uphill battle getting to hike just once or twice despite the current market pricing, but the US Bureau of Labour Statistics (BLS) decided to overshadow that narrative yesterday.

First of all, we have namely received an important inflation update over the past week, and this is admittedly one for the nerds. I know most you won’t care, but this technical revision matters as it carries an essential medium-term significance for inflation levels on both sides of the pond. The US CPI weights have been updated based on consumer expenditure data from 2019-2020, which means that the statistical bureau has looked at the actual spending over the past years and updated the “consumer basket” on the back of it.

So, what happened in practice, when the BLS updated the weights of the CPI index yesterday?

The simple and most practical example I can give you of the updated consumer basket is the following:

The weight of "food away from home" in the consumer basket is materially down (a service)

The weight of "food at home" in the consumer basket is materially up (a good)

This is solely a result of the pandemic and the restrictions imposed consequently. Goods will increase in significance in the CPI index, while services will decrease in significance accordingly. A natural consequence of the lock-down policies pursued in most parts of the world during parts of 2020.

Goods prices are generally more flexible than service prices, why the pandemic surge in goods consumption (and the accordingly distressed supply chain) led to a massive spike in inflation when everyone and their mother requested a bunch of goods at the same time since services were (partly) locked down.

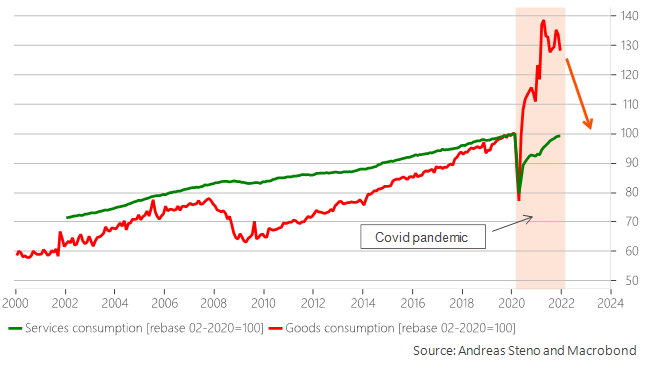

Chart 1. The Covid pandemic led to a bizarre increase in goods consumption –> inflationary! Will it reverse soon?

If restrictions are now more permanently being lifted (my base-case), we should expect goods consumption and maybe also prices to drop, which should now matter even MORE given that goods have been given a higher weight in the newly updated consumer basket.

The changes made by the BLS hence provide a net/net negative impact on inflation down the line (likely during H2-2022 already), but not before another positive tilt to inflation is seen in the very short-term.

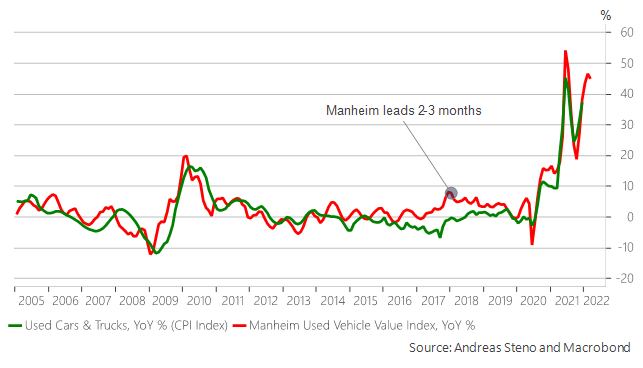

Used cars & trucks prices are going to re-accelerate short-term according to the solid Mainheim indicator and the category has been given a larger weight in the annual re-weighting due to extraordinary purchase volume of used cars due to delivery shortages on new cars. This is one reason to expect (core) inflation to surprise to the upside tomorrow (Thursday).

The bottom-line of the new technical update (it by the way happens every year, so please take off your tinfoil hat by now) is that inflation will likely go further up during Q1, but consequently head SHARPLY down in Q2-Q4, which is a trend that will be emphasized by these new weights in the CPI index.

Chart 2. Inflation will head further north in Q1 due to the new weights, but Q2-Q4 will see big disinflation

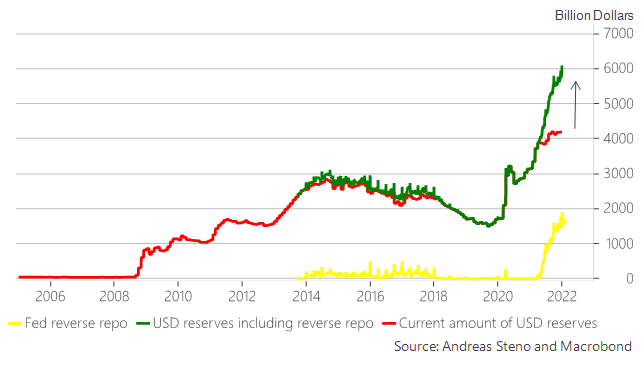

Ultimately, I stick to a more benign outlook for bonds and tech-stocks from Q2 an onwards and I don’t really fear the planned QT from the Fed in that regards either. We will not see a strong negative USD liquidity effect from QT initially as the gap between the total amount of printed USD reserves and the current amount of USD reserves available to the banking system will act as a buffer once the Fed starts bringing down the balance sheet size (QT). Why is that?

Currently, a lot of reserve USDs are parked at the reverse repo (almost 2000bn) due to a lack of alternatives (read, no yields on short-term instruments such as T-bills). QT will likely almost immediately start creating those alternatives again, why USD reserves currently parked at the reverse repo will flow into T-bills once QT commences effectively leaving USD liquidity unchanged as frozen reverse repo liquidity will be unleashed in to the system. This is going to help mitigate the adverse effects of the Fed trying to bring down the balance sheet size again, and this is in sharp contrast to the QT process of 2017-2018 when such a mitigating factor was not in place.

Chart 3. The difference between QT in 2022 and 2017 is the big amount of idle USDs parked at the reverse repo

Could you comment on the Saudis continuously pricing oil higher which is helping push inflation. Plus, if the Fed add 1% to prices by July 1st as Bullard expects how will CPI fall dramatically?

I really enjoyed reading this, thank you!