Steno Signals #58 - The one on banana republics, yield curve controls and the yuge EUR consensus among asset managers

We are now one step closer to a normalization of the monetary policy in Japan and I guess it is safe to say that the only thing that is normal in this cycle is that monetary policy returns to "normal"

Happy Sunday and welcome to our flagship editorial!

What a bizarre week it has been in global macro. The outlook for the economy, rates, fx and other assets apparently never fails to surprise!

We have thankfully made very decent returns through a tough trading week as some of our cyclical rotations had a tremendous start to the week before taking a minor hit when the change of the yield curve regime in Japan was announced.

First things first. The decision to move the cap in the 10yr point of the Japanese Government Bond (JGB) curve from 0.5% to 1.0% was a big surprise to many timing-wise. Market participants had discussed this move from the Bank of Japan in length over the past months, but most people seemed to conclude that it was a decision for later. We have continuously flagged this risk through the past quarters, but also highlighted how such a decision had to come as a surprise to work its magic. And so it was (a surprise) – at least almost.

Hilariously, the regime shift was already leaked to Nikkei a day ahead of the actual decision, which is worthy of an award for the “banana republic of the week” to Japan and its monetary authorities.

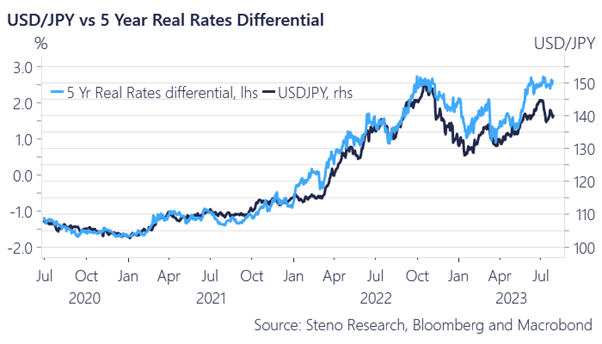

Chart 1: USDJPY still looks too low despite the recent move by the BoJ

On a more serious note, we find it problematic for FX, equity and rates bets in Japan that the fiscal- and monetary authorities apparently cannot keep tight ahead of such an important policy announcement.

The JPY has already lost all of its gained announcement effect versus the USD again, likely as 1) the information leak is considered EM-like in nature and 2) the fundamental JPY case remains unbacked by rates in both nominal- and real terms despite the move from the BoJ.

Nominal rates in USDs have actually moved more than peers in JPY in the wake of the announcement as the market digests the ambiguity of the flexibility introduced to the yield curve control from the BoJ.

There is now a firm line in the sand at 1%, but the BoJ may at any point in time decide to intervene to dampen rates between 0.5% and 1.0% (or potentially 0% and 1%), if they find a yield spike unwarranted. This is toxic for the speculative crowd as it is not cheap to bet against the BoJ as we and others have already experienced this year. First, carry is against you in all Japanese macro-based bets (in JGBs and JPY at least) and second, you are betting against a potential bazooka. If anything, the right bet is probably to follow the path of Mr Buffet and buy Japanese financials on a bet of a steeper yield curve in JPY.

So far, the market is very far from trying to test the BoJs resolve to defend the new 1% threshold, and we are not convinced that markets will try to chase rates even close to such levels unless they get the green light to do so rhetorically from the BoJ. There is literally still blood on the streets after the last couple of attempts at chasing the long JPY / short JGB trade back in January and February, and the widow-maker trade of the year very early found a clear front-runner in Japan in sharp competition with the bearish equity position.

The two-way market in JGBs is finally back!

Chart 2: The introduced flexibility may be a smart move from the BoJ as it removes the procyclicality of the current monetary policy

Keep reading with a 7-day free trial

Subscribe to Stenos Signals to keep reading this post and get 7 days of free access to the full post archives.