Steno Signals #125: EUR Liquidity Overtakes USD Liquidity – A Historic Shift

We are writing history at the moment as EUR liquidity is getting more sought after than USD liquidity....

We are writing history at the moment as EUR liquidity is getting more sought after than USD liquidity. This is a rare event in financial markets, and probably also a sign that the ECB is about to take it too far with QT.

Happy Sunday from Copenhagen.

Bear with me this week through this long read as we approach an extremely interesting crossroads in sovereign bond markets, impacted by very tight liquidity. This story has been somewhat masked by policy events in the US and Germany, but it may nonetheless be the most important narrative for Q4, which is why you need to pay attention to it.

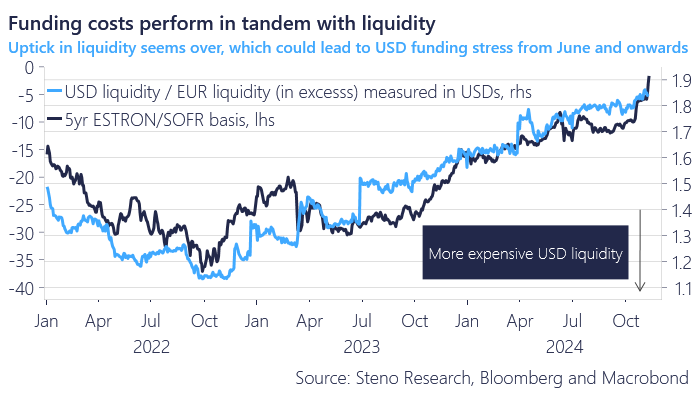

We are witnessing history being made in several significant ways, with Bunds trading through swaps and ESTRON/SOFR cross-currency swaps approaching zero across the curve. This combination is unprecedented in modern financial history and is highly indicative of the current market sentiment surrounding the QT programs run by the three major central banks. They will need to slow down QT soon, or markets will push back even more than we have already seen.

This is a strong signal that the ECB’s QT is now more painful than the Fed’s. The Federal Reserve still has tools such as the ON RRP facility to counter liquidity trends, and soon the TGA will add reserves to the system as the debt ceiling deadline approaches.

Chart 1: EURUSD xCCy basis close to trading above 0 for the first time in a LOONG while..

In contrast, EUR liquidity could become more in demand relative to USD liquidity (with cross-currency basis closing in on zero), which would be historically significant and a strong indication that the ECB needs to respond promptly. However, they are unlikely to take swift action, as the ECB is a reactive central bank by nature and may not yet be fully attentive to these developments.

It will be interesting to observe how poorly Bunds may trade in the coming months as the ECB plans to double down on liquidity withdrawals by ramping up PEPP QT in 2025. There is a clear risk of an outright crisis in European debt markets as a consequence.

Meanwhile, high beta markets such as crypto and some equities have picked up on this, leading to a repricing of the future outlook for liquidity, which has turned into a very bullish scenario. We think these markets are onto something and also expect a swift U-turn from central banks in the coming 1-2 quarters in support of the bond market/debt reset, as the current bond yields are hard to sustain for politicians looking for ways to stimulate.

If central banks decide to underpin the sovereign bond markets in response to these developments in asset swaps, liquidity trends and xCcy swaps, it is an exceptionally bullish back-drop for debasement bets such as Crypto, Gold and Technology (again).

Read more below to understand why this is happening and why it matters.

Chart 2: Sovereign bonds such as Bunds are trading at historical extremes versus swaps

An asset-swapped Bund is a purchase of a German Bund bundled with an interest rate swap with an opposing return profile, meaning that the spread between the two depicts the difference between the yield on a German government bond and the corresponding yield/rate set between two dealers in the interbank market for EUR interest rates.

These asset swap packages are particularly favored by hedge funds as they are typically very stable and therefore easy to leverage, given the relatively low value at risk associated with these positions. Buying Bunds versus the interest rate swap is generally seen as a reliable hedge in times of turmoil, as the Bund is the best collateral available in the Eurozone outside of cash reserves. Bunds also typically outperform swaps when needed most. However, we have recently observed a breakdown in the performance of Bunds relative to swaps, even as German equities have shown weakness—precisely the scenario where you do not want this trade to fail.

This is symptomatic of bond markets lacking the central bank bid that we became accustomed to during the 2010s and the pandemic. If viewed pessimistically, one could argue that this signals a repricing of sovereign debt risk relative to banking credit risk, which is clearly a warning sign.

Chart 3: Debt servicing costs in the US exceed pain thresholds

Keep reading with a 7-day free trial

Subscribe to Stenos Signals to keep reading this post and get 7 days of free access to the full post archives.