JAPAN WATCH – THE YCC TIME BOMB FOR WESTERN FIXED INCOME

Japan is as MUST watch as a risk taker as the potential scrapping of the YCC policy holds true time bomb potential for Western markets. Here is what is currently priced in and how to position for it.

Steno Signals has MOVED. If you want to join the Steno Research family, you can subscribe here → https://stenoresearch.com/subscribe/

“Either you do Japan, or else Japan will do you.” Anonymous Danish Fixed Income PM

As a part of our increased focus on inflationary pressures spilling over from the West to Asia, we have of course kept an eye out for who BoJ’s next governor is going to be. Yesterday, it was finally formally announced that prime minister Kishida and the Japanese government will replace current governor Kuroda with ex BoJ member and economics professor Kazuo Ueda on the 8th of April.

Ueda the new BoJ governor – who is he?

Surprisingly enough, Ueda wasn’t a part of the list of likely candidates for the role that was published in newspapers and media around the world, so most analysts got a big surprise in their inbox Friday. The election comes in a period where Prime Minister Kishida’s support is around record lows, so he and his administration have been busy finding the perfect candidate – one that’s dovish enough so that the LDP (Liberal Democratic Party) wouldn’t be left split – and hawkish enough such that they can keep control of inflation and get Japan back on track.

Reportedly Kishida wanted Amamiya, but he declined and recommended Ueda – in short because he wants an “actual economist” to review and possibly change the monetary regime that Amamiya built. Interestingly a source revealed that Amamiya said that “the next BOJ leadership has to review and amend yearslong monetary easing..” The new governor is clearly tasked politically with the design of a NEW strategy, which includes an amendment of the YCC program.

Ueda comes with a bit of both. He’s more hawkish than the previously favored candidate Amamiya, and has criticized the BoJ multiple times for their prolonged ultra-loose monetary policing, which according to him hasn’t pulled Japan out of their deflationary and economically stagnating regime, and their lack of medium-term guidance. However, don’t expect him to be ultra-hawkish and pull the entire carpet within a blink of an eye. Ueda has previously advised the BoJ to be careful about raising rates as soon as the 2% inflation target has been exceeded, and in his time in office he voted against a rate hike proposal. Hence, expect a potential reversal of the stimulus programme to be fairly slow, but maybe also a new tone in the meeting minutes.

Let’s dig into how big of an impact the BoJ governor really has, and what it could mean relative to the current market pricing.

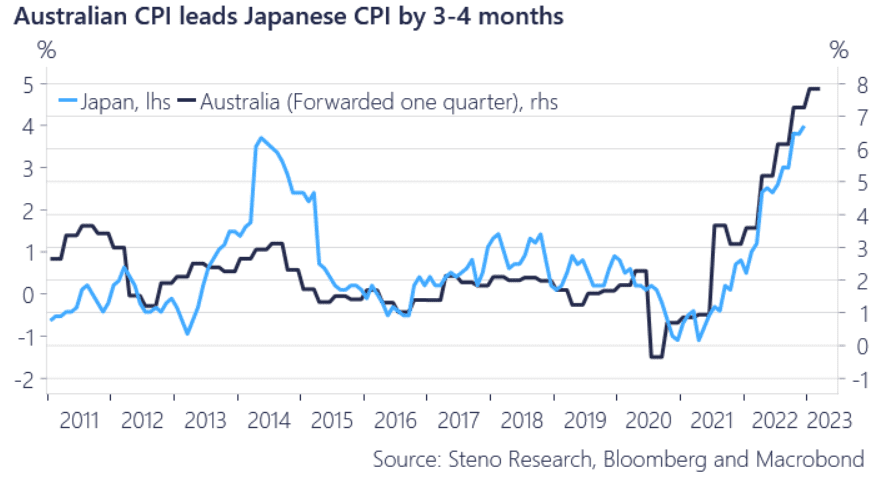

The inflation picture will likely turn even hotter in Japan in coming months making this matter urgent for investors in the West.

Chart 1: Lagged Australian CPI vs Japanese CPI

To get access to the entire Japan Watch and how we assess the pricing of outcomes, you need to be a client of Steno Research. Find out how to join the family below.

Step by step: How to become a part of the Steno Research team?

1. Choose one of our offered subscription-packages

Basic: Gives access to Steno Signals, The Great Game and Five Things We Watch

Premium: Gives access to all of the above, all Watch-series (detailed knowledge on asset allocation) AND our dynamic data-dashboard with price models and asset allocation strategies across assets when it is launched shortly.

2. Subscribe here → https://stenoresearch.com/subscribe/

If you have questions or want to buy a package of licenses and/or live access to the analyst team for your company or institution, please contact info@stenoresearch.com

Not gonna happen. Japan GPD is growing less than potential.